When discussing 2023 inflation trends, we first take a look back at the Federal Reserve’s recent moves regarding interest rates. Last month, the Federal Reserve raised rates by 25 basis points. This stepped down from 50 basis points in December. However, the latest strong batch of economic reports suggest that 50 basis points returned to the table.

Examining the Future Beyond 2023 Inflation Trends

Regardless of whether the Federal Reserve raises rates by 25 or basis points, investors need to ask themselves about where the United States economy will head over the course of the next 6-12 months. Furthermore, what does the terminal rate look like for interest rates? Will it be 4.75%, 5.0%, or 5.25? Currently, any of these numbers is in play. Additionally, most fixed-income investors should feel capable of handling these rate increases.

However, in the event that the Federal Reserve feels the need to increase the federal funds rate beyond 5.25%, this causes greater challenges for investors and the United States economy as a whole. Rates at 6.0% and 6.25% create more cause for concern.

Understanding the Federal Reserve’s Inflation Strategy

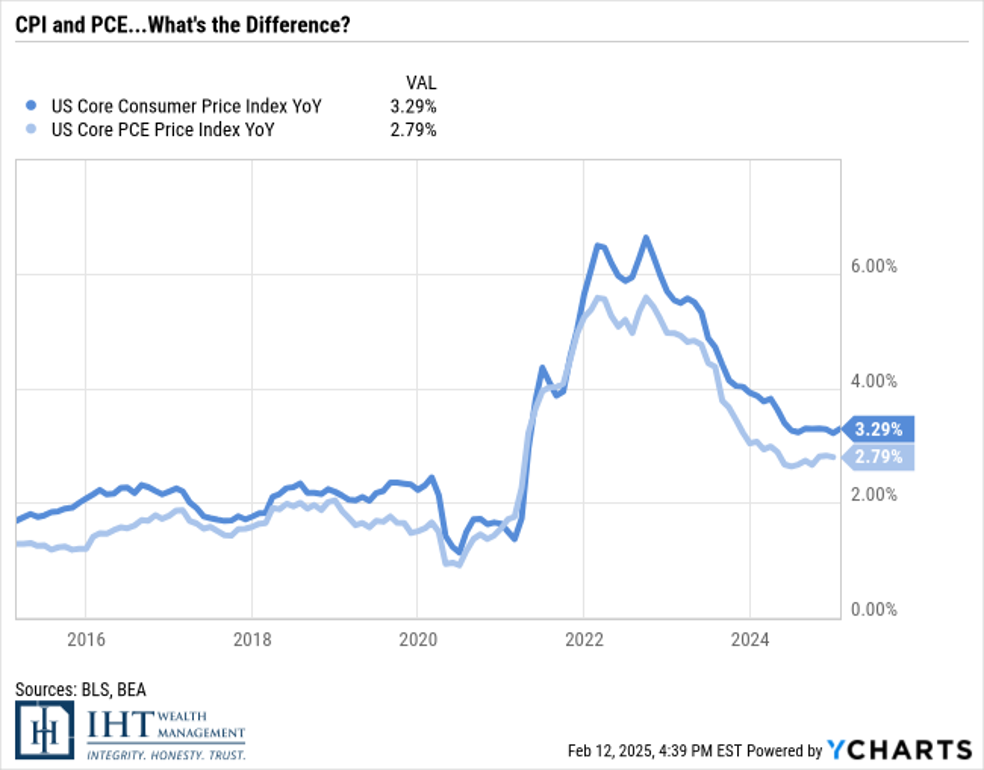

This past week, the Produce Price Index, inflation figures, and consumer spending figures came in stronger than anticipated. For instance, the Producer Price Index rose 0.7% month-over-month in January. This exceeded the 0.4% increase consensus forecast. Ultimately, this data does facilitate concerns over the “stickiness” of inflation.

Overall, the Federal Reserve’s hands are somewhat tied. Not only are they combatting inflation, they are dealing with expectations of future inflation as well. Food prices, fuel prices, and other volatile market sectors contribute to higher inflation expectations. In another example, housing prices facilitate further inflation. Since the Great Recession, the United States dealt with a shelter shortage. To make matters worse, raising interest rates further increases prices related to home construction, skilled labor, and material costs.

Best Practices for Dealing with 2023 Inflation Trends

Despite these challenges, inflation will eventually come down. At present, the economy is facing a lag effect from the Federal Reserve’s periodic rate increases. Even by the end of 2023, it is unlikely that the Federal Reserve will begin to cut interest rates due to this lag effect. Crucially, the Federal Reserve wants to “beat” inflation the first time around, as opposed to pausing or scaling back interest rate hikes only to redo them later down the road.

In the meantime, the bond market should see plenty of activity, making banking stocks and investing vehicles attractive. Simply put, they do not face the same wage pressure that other sectors, like restaurants and bars might. As for the ongoing concerns regarding the tech sector, this market segment proved time and time again to find new ways to drive margins, even in tough times.

Watch the full interview on YouTube.

To reevaluate your inflation strategy in 2023, contact the financial advisors at IHT Wealth Management.