Pulling Back The Curtain On The AI SaaSpocalypse

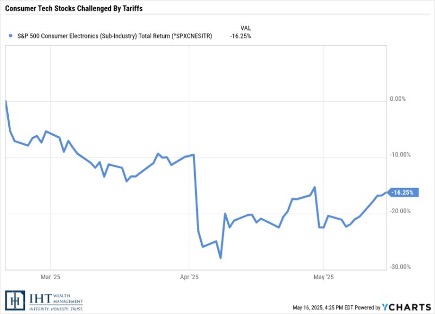

Fear that artificial intelligence will render traditional software subscriptions obsolete has driven a broad and, in many cases, deeply indiscriminate selloff across the software sector. Companies with strong fundamentals, sticky customer bases, and genuine AI integration strategies have been marked down alongside those with legitimate structural vulnerabilities. It’s a classic case of sentiment-driven dislocation rather than rational repricing. For investors willing to look past the noise, the current environment is shaping up to be exactly the kind of moment where long-term opportunities can appear.

What is less discussed is how that same anxiety is now rippling through the roughly $3 trillion global private credit market, which spent the better part of a decade lending aggressively to the same software companies now under pressure in public markets. Headline risks in the space have risen, investment gates have come up, and some retail investors are scrambling to try to pull their capital out. We firmly believe the risks for the space need to be put in context: private credit has always been a high-yield, higher-volatility asset class, and investors who understood what they were buying have historically been well-compensated for accepting that risk.

The current stress is a feature of the asset class and one of the primary reasons why yields in the space have generally outpaced those in the public markets.

How Private Credit Ended Up At Odds With AI

The rise of private credit over the past decade is one of the defining financial trends of the post-GFC era. As traditional banks retreated from middle-market lending following the GFC, a new class of non-bank lenders rushed in to fill the gap. Business development companies, or BDCs, became the vehicle through which much of this capital was channeled and became widely available to retail investors. Private credit, an asset class historically reserved for institutions, became available to the masses.

The pitch was compelling. Private credit offered yields that dwarfed what investors could get from public bonds or money market funds, with relatively muted volatility given that these loans don’t trade on public exchanges. The absence of daily mark-to-market pricing meant the asset class felt stable even during periods of public market turbulence. Capital flooded in. The private credit market has ballooned from roughly $500 billion a decade ago to $3 trillion today.

And where did a significant portion of that capital go? Software. The thesis was intuitive at the time. SaaS companies offered lenders exactly what they wanted: recurring revenue, sticky customer bases, scalable platforms, and asset-light business models that had historically supported strong repayment rates. Deals got done, but loans originating prior to 2024 largely failed to contemplate artificial intelligence as a meaningful business risk.

AI Impact: Cracks in the Foundation

AI disruption fears quickly hit software stocks in public markets late last year, but the damage wasn’t immediately visible in private credit. That’s by design – privately held loans don’t reprice the moment sentiment shifts. But the stress has begun to surface. The first signals came from the equity prices of the major alternative asset managers themselves. Firms running large private credit franchises saw their stocks fall sharply in a matter of days, even as the broader market barely moved. The market was repricing not just the software borrowers, but the entire credit infrastructure behind them.

Then came the redemptions. Several of the largest non-traded BDCs and interval funds began receiving withdrawal requests at rates far beyond what their quarterly redemption structures were designed to handle. When requests arrived above the standard 5% quarterly cap, funds were left with an uncomfortable choice: honor what they could and gate the rest or sell loans at a discount into a stressed market to meet demand. Most chose the gate.

In the first quarter of 2026 alone, investors across the non-traded BDC landscape requested nearly $14 billion in redemptions. Sponsors honored roughly half. That gap is real, and it reflects the inherent tension in offering semi-liquid access to an illiquid asset class. It is also, importantly, not without precedent; prior stress cycles in private credit produced similar dynamics before the asset class stabilized and investors who stayed the course were rewarded.

Context Matters For AI Disruption

The structural challenge runs deeper than sector concentration alone. Many of these loans carry five- to seven-year maturities, meaning businesses that appeared insulated from AI disruption at origination may face a very different competitive landscape by the time those loans come due. Forecasting the long-term impact of a technology transition across hundreds of individual borrowers simultaneously is an underwriting challenge that private credit has not faced before at this scale.

However, it would be a mistake to look at the current turbulence in private credit and conclude that the asset class has failed its investors. The more accurate reading is that it is being stress-tested – and that the outcome of that test will depend heavily on how portfolios were constructed.

Some of the more credible stress scenarios that we have seen put potential default rates at roughly 8%- 10% in a moderate AI disruption environment. That figure sounds alarming in isolation, but the math on recovery rates and coupons is a bit more forgiving. Defaults don’t mean complete wipe outs; there’s usually residual value in the business, and most loans are written with healthy equity buffers in place. Furthermore, the high coupons from the loans mean that even during periods of stress, there’s still income flowing into the portfolio.

A simplified example: an unleveraged portfolio with a 10% default rate would have lost its clients 10 cents on every invested dollar. If the remaining 90% of the portfolio pays 10%. That puts the portfolio back at 99 cents on the dollar. Then, if there’s some residual value in the loans that defaulted – say the company went to liquidation and each of the loans saw a 50% recovery rate, that gets another 5% of the portfolio back. The portfolio is back in positive territory and ended up making 4%, even with defaults.

To be clear – there are a lot of assumptions in the above scenario; leverage, fees, lower recovery rates, and several other factors could all make your situation a lot worse. You can absolutely lose money in these vehicles.

But, for investors who entered private credit with a clear-eyed understanding of what they owned – illiquid loans to middle-market companies, priced on an appraisal basis, accessible only on a quarterly basis subject to caps – the current environment is functioning as disclosed. The yields that attracted capital to the asset class in the first place were not an accident. They were compensation for exactly this kind of risk. Volatility, in private credit, is not a sign that something has broken. It is a feature of the asset class that has historically been well worth tolerating.

What This Means for the Retail Investor

For retail investors currently holding exposure to private credit through BDCs or non-traded vehicles, the most important priority is understanding what is actually inside the portfolio. Not every private credit manager is equally exposed to software risk, and not every software borrower is equally vulnerable to AI disruption. There is a material difference between a well-underwritten loan to a profitable enterprise software company with a decade of customer relationships and a leveraged buyout loan to a mid-market SaaS company accruing interest it cannot pay in cash – a structure known as payment-in-kind, or PIK.

The same logic applies on the equity side. The software companies best positioned to weather this moment are those that have spent the past several years building AI into their platforms. Enterprises don’t abandon the software infrastructure they’ve spent years integrating overnight – switching costs are real, institutional data doesn’t migrate cleanly, and the trust built between long-standing vendors and their customers isn’t easily replicated by a new AI tool. That dynamic tends to favor large, deeply embedded platforms like Microsoft (MSFT) or Salesforce (CRM), both of which are aggressively integrating AI into existing workflows rather than trying to rebuild them from scratch. The case for a company like Adobe (ADBE) may be more balanced. On one hand, Adobe sits directly in the line of disruption, with image generation, content creation, and photo editing increasingly being replicated by emerging AI tools. On the other, its products remain deeply embedded in global creative and enterprise workflows, creating switching costs that are difficult to displace overnight.

The selloff has also created dislocations further down the market cap spectrum. Firms like ServiceNow (NOW) and HubSpot (HUBS) have seen multiple compression despite continuing to grow into mission-critical layers of enterprise software stacks. The market is currently pricing these businesses as if disruption is inevitable, when in many scenarios they could actually become beneficiaries of AI adoption.

The current selloff looks far more like a sentiment-driven entry point than a structural unraveling. That does not mean every software company will emerge unscathed, but it does suggest that indiscriminate selling is creating pockets of mispricing. For investors able to differentiate between durable platforms and speculative business models, this is the kind of environment where long-term positions can be built.

The Only Certainty Is AI Persistence

Pull back far enough and a coherent narrative emerges from what can feel like two unrelated dislocations. A decade of near-zero interest rates pushed capital into the far reaches of the risk spectrum. Software, with its recurring revenues and high margins, became the consensus answer for investors across every asset class – public equity funds bought the stocks and private credit funds underwrote the debt.

When AI disruption began to challenge that thesis, the repricing started where prices are most visible: in public equity markets. But the same recalibration is now working its way through the credit stack, repricing the debt that financed the same companies whose equity has already been marked down. The difference is that in private credit, that repricing is happening slowly and through mechanisms – redemption gates, PIK accruals, covenant amendments – that are less visible to most retail investors than a declining stock price.

The software selloff and the stress building inside private credit are ultimately expressions of the same underlying question: how much of what we believed about software’s durability turns out to be true in an AI-powered world?